Key event risk of the week: Markets eyeing US CPI inflation

Market consensus

Year on year –

Headline: Estimate: 3.4%; Previous: 3.2% (Estimate Range: 3.5% High; 3.1% Low).

Core: Estimate: 3.7%; Previous: 3.8% (Estimate Range: 3.8% High; 3.5% Low).

Month on month –

Headline: Estimate: 0.3%; Previous: 0.4% (Estimate Range: 0.5% High; 0.2% Low).

Core: Estimate: 0.3%; Previous: 0.4% (Estimate Range: 0.4% High; 0.2% Low).

Bloomberg estimates

Undoubtedly, March’s US CPI inflation release is the headline event this week, scheduled to hit the wires at 1:30 pm GMT+1 tomorrow. Traders and investors will look to the inflation print to determine the Fed’s next move. As you can see from the above, nominal headline inflation (YoY) is expected to tick higher in the month of March, underpinned by a rise in energy prices. The core measure, which strips out energy and food components, is set to cool further to 3.7%, which would mean a new three-year low for the rate.

What are we hearing from the Fed?

With headline and core inflation poised to remain sticky, the Fed has made it abundantly clear that its focus is on inflationary pressures in making decisions about easing policy.

The Fed Chair Jerome Powell has noted that until there is more confidence regarding the inflation picture, he does not envisage the Fed cutting rates. However, he did note that he still believes it will be ‘appropriate’ to cut rates at ‘some point’ this year. What is interesting is that Powell also highlighted that recent economic data do not ‘materially change the overall picture’ and that it is too soon to say whether the recent acceleration in inflation is more than a ‘bump’. Time will tell on that one!

On the other side of the fence, nonetheless, some Fed officials underline a scenario where the Fed does not cut rates at all this year. Minneapolis Fed President Neel Kashkari recently commented in an interview with Bloomberg TV: ‘If we continue to see strong job growth, if we continue to see strong consumer spending and strong GDP growth, then it raises the question […] why would we cut rates’.

We also had Former Federal Reserve Bank of St. Louis President James Bullard hitting the wires recently. Speaking on Bloomberg TV, Bullard communicated that three rate cuts this year is the ‘base case’ and made note that this is the Fed’s ‘best guess right now’.

The overarching perception derived from all the Fed Speak in recent weeks is that the Fed is not in a rush to cut rates. This has seen UST yields push higher, with investors betting that rates will remain restrictive for longer this year.

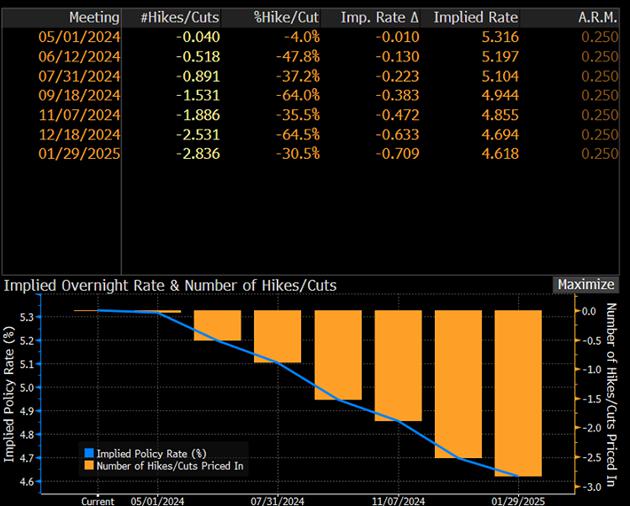

Ahead of the event, the swaps market is pricing in just -63bps of easing for the year, which, by anyone’s standards, is quite the deviation from the beginning of the year when the market was ambitiously forecasting around -150bps of cuts. June’s policy meeting remains on the table for the first 25bp cut (-13bps), but July is looking more of a solid bet (-22bps).

Also, as a reminder, we’ll be welcoming the minutes from the latest FOMC meeting at 7:00 pm GMT+1 tomorrow as well.

Trading the CPI report

Should the report see a broad miss in the data, US yields will likely slump, as will the greenback, though gold and stocks should punch higher. You’ll also perhaps see a dovish repricing in rates, placing July firmly in view as a meeting to watch, maybe even June.

Nevertheless, a higher-than-expected print could bolster demand for the USD and see yields rally. Conversely, gold and stocks are likely to take a hit in this case.

The US Dollar Index will be an interesting watch leading up to the release. As illustrated in the daily chart below, we’re tentatively working below resistance at 104.15, which paves the way lower to the 200-day and 50-day SMAs at 103.80 and 103.92, respectively. Between here and the support below at 103.62, this could be an area of support tested/respected in the event of a beat in data. However, softer numbers could see the unit voyage south of the support and open the door for a bearish scenario to support at 102.92.

Reprinted from FXStreet,the copyright all reserved by the original author.

Disclaimer: The content above represents only the views of the author or guest. It does not represent any views or positions of FOLLOWME and does not mean that FOLLOWME agrees with its statement or description, nor does it constitute any investment advice. For all actions taken by visitors based on information provided by the FOLLOWME community, the community does not assume any form of liability unless otherwise expressly promised in writing.

FOLLOWME Trading Community Website: https://www.followme.com

Hot

No comment on record. Start new comment.