Crude oil prices fell by 4.24% yesterday. They have been continuously declining for five consecutive days since last Monday. Although there was a slight rebound in prices one day in between, the overall oil price has still dropped from $74.78 to around $67. On June 4th, OPEC+ announced an extension of production cuts, and the oil price experienced a gap-up at the opening on Monday. When the market believed that oil prices would rebound, crude oil prices continued to fall. The effect of production cuts on boosting oil prices seems to be not significant. In addition, factors such as severe wildfires in Canada, Russia's voluntary extension of production cuts, and the ongoing El Niño warm current have been announced, but they have failed to push oil prices up. Therefore, we need to look at what reasons have greatly overshadowed the bullish factors mentioned earlier and caused oil prices to not only fail to rise but also continue to fall.

1. Weak economic data from major Asian countries

Last Friday, China released its May Producer Price Index (PPI) year-on-year, with a published value of -4.6%, lower than the forecast value of -4.3% and the previous value of -3.6%. It also released the Consumer Price Index (CPI) year-on-year and month-on-month for May, with a year-on-year value of 0.2%, the same as the forecast, but the month-on-month rate of -0.2% slightly lower than the forecast of -0.1%.

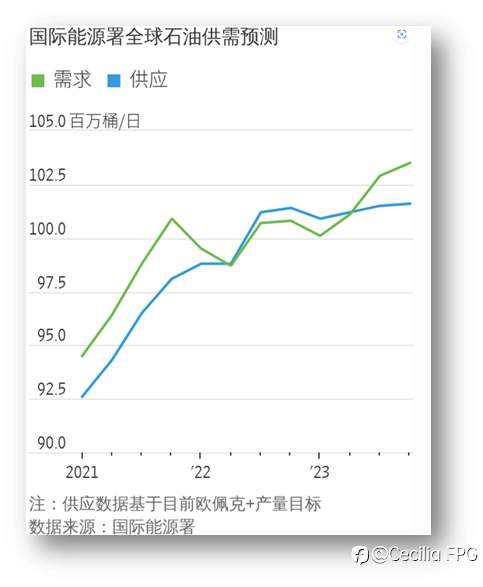

On February 15th of this year, the International Energy Agency (IEA) raised its expectations for oil demand to a new historical high of 110.19 million barrels per day. Compared to before, this year's oil demand is expected to increase by 2 million barrels per day, with 1.4 million barrels coming from Asian countries and China alone accounting for 900,000 barrels per day. The IEA stated that China's resumption of control measures related to the COVID-19 pandemic and the reopening of international tourism borders in Asian countries are likely the main reasons for the upward revision of demand expectations. After lifting control measures, China is expected to resume its role as the main engine of global oil demand growth.

However, based on the data from last Friday, China's PPI year-on-year declined by 4.6%, marking eight consecutive months of decline and reaching the largest drop in seven years. This data indicates that international commodity prices, as a whole, declined in May, and there was weak demand in the domestic and foreign industrial goods markets. Consumer concerns about the development of the economic outlook can lead to a decline in demand for crude oil. As the major Asian country supporting the growth of oil demand, this data will undoubtedly put pressure on the rise in oil prices.

2. Lack of transparency in Russian crude oil export data

This Monday, India announced that the May Consumer Price Index (CPI) year-on-year rate was 4.25%, lower than the previous value of 4.7% and the forecast value of 4.42%. However, the industrial output year-on-year rate and manufacturing month-on-month rate showed significant improvement. These data indicate that India's industry and manufacturing sectors have entered a phase of substantial development. On the other hand, according to the Indian Economic Times, based on data from Vortexa, an energy commodity tracking agency, India imported more crude oil from Russia in May than the combined imports from Saudi Arabia, Iraq, the United Arab Emirates, and the United States, reaching 1.96 million barrels per day, a 15% month-on-month increase compared to April. Russian crude oil accounted for nearly 42% of India's total crude oil imports in May, while the proportion provided by OPEC+ dropped to a historical low of 39%. Vortexa analyst Serena Huang pointed out that the total trading volume for June and July is expected to continue to rise.

Based on reports from analysis companies in April, the price provided by Russia was $68.21 per barrel, while Saudi Arabia was $86.96 per barrel, and Iraq was $77.77 per barrel. There is no available data for May prices, but based on the preceding transaction amounts, it is certain that the price offered by Russia is significantly lower than that of countries like Saudi Arabia. The substantial reduction in the cost of crude oil imports provides a boost to India's industrial sector, and the ongoing growth in manufacturing capacity will drive up India's demand for crude oil.

A month ago, Russia stated that it would temporarily not disclose its crude oil export data. In April, the market began to doubt whether Russia was actually reducing production as agreed, as its continued increase in export volume seemed contradictory to the commitment to production cuts. However, it was also considered that these exports could be for inventory clearance since the mild winter in Europe had led to a decrease in oil demand. Russia may have accumulated a significant amount of crude oil inventory, so even if production cuts were announced, the effects would only be seen after the inventory clearance. However, due to Russia's suspension of the publication of relevant export data, tracking institutions can only roughly estimate Russian crude oil exports based on observations of shipments at sea or entering ports. Currently, it appears that Russian offshore crude oil exports remain at high levels and are slowly increasing, which is frustrating for OPEC+ member countries. As of June 4th, the average offshore crude oil export volume from Russia for the past four weeks has risen to 3.73 million barrels per day, higher than the revised level of 3.68 million barrels per day on May 28th.

Therefore, we can suspect that Russia may not actually be reducing production. If, while OPEC is implementing production cuts, Russia is secretly selling to major energy-demanding countries in Asia at lower prices and increasing its output, it will undoubtedly heavily suppress the effectiveness of OPEC's production cuts. After the recent OPEC+ meeting in Vienna, Saudi Energy Minister Prince Salman mentioned Russia and stated that they requested Russia to clarify its data and reinforce transparency regarding its crude oil production figures.

However, from my perspective, firstly, Russia is currently in a relatively tense situation. The sustained pressure from various countries is having a significant negative impact on its domestic economy. The continued growth in India's demand capacity can provide some buffering to the Russian economy at this time. So, if Russia were to reduce production at this time, unless they can find more ways to boost their economy, the temptation to increase production would be strong. Additionally, if they are indeed adhering to production cuts as agreed, it is difficult to understand the reason for choosing not to disclose the data.

Therefore, we can suspect that this is one of the main reasons suppressing the rise in oil prices.

3. Implementation of a soft landing in the US economy

Another key time point is the initial jobless claims in the United States, which were announced last Thursday at 8:30 PM Beijing time (10:30 PM Australian time). The reported value was 26.1, significantly higher than the previous value of 23.3 and the forecast value of 23.5. Within three hours of the announcement, crude oil prices dropped by 5%. This data indicates an increase in unemployment in the United States and suggests that the US economy is slowing down as anticipated by the Federal Reserve. The next release of unemployment rate figures is also expected to rise accordingly. However, on the other hand, it also indicates that the US economy may be entering a downward trend in the second half of this year. The economic downturn has led to increased market concerns about the future, resulting in a decrease in demand for crude oil in both production and daily life. Additionally, as crude oil is priced in US dollars, the weakened US dollar also contributes to a decline in oil prices. Therefore, at the time of the initial jobless claims announcement, concerns about the US economic outlook combined with a declining US dollar dealt a double blow, leading to a significant decline in oil prices.

As the economy of the most important economic powerhouse faces a downturn, major Asian countries' economies underperform expectations, and the majority of the market is dominated by Russia, while the Eurozone continues to invest in the development of new energy sources and faces economic pressure from high inflation in European countries, the global crude oil market is currently overshadowed by uncertainties.

If no signals that stabilize oil prices emerge later on, and considering the overall market downturn that has caused oil prices to fall below $70 despite the temporary price increase after the OPEC meeting on June 4th, it will be challenging for oil prices to rebound in the short term.

It is also worth mentioning that major oil-producing countries like Saudi Arabia are starting to consider shifting some economic focus. This year, OPEC stated that oil prices need to be above $80 for a balanced budget. If prices remain low around $70 in the long term and there are no additional economic drivers, it will pose a crisis for the economies of OPEC+ member countries.

Based on the 4-hour trend chart of crude oil, the current price is testing the support level around $67.5. After a few days of decline, the bearish momentum has slightly weakened. Although the downward pressure on the overall market remains, indicators such as Stochastic and RSI suggest that there will be a period of oscillation and rebound in the short term. The rebound could target around $70, but due to the impact of fundamental factors, the overall price trend is likely to continue to decline. If the oil price falls below the support level at $67, the next support level will be around $65.

In conclusion, personally, I would choose to take a long position around $67.5 to capture profits from the price rebound. If it can rise to around $70, I would then assess the market signals. If no further signals emerge, I will sell at that point and switch to a bearish view on crude oil.

Disclaimer: The views expressed are solely those of the author and do not represent the official position of Followme. Followme does not take responsibility for the accuracy, completeness, or reliability of the information provided and is not liable for any actions taken based on the content, unless explicitly stated in writing.

Leave Your Message Now