#OPINIONLEADER##OPINIONLEADER#

Markets are staying in risk aversion today with heavy selling in stocks. Expectations on the negotiation between Ukrainian President Volodymyr Zelenskyy and Russian President Vladimir Putin are low. Meanwhile, other markets are relatively steady. In forex, Swiss Franc, Yen and Dollar are still the stronger ones ,while Euro is the weakest. But still, most pairs and crosses are staying inside last week’s range.

Technically, commodity currencies are rather resilient in the risk aversion environment. If sentiment improves, there are prospects of further rally. Attention will be on 0.7282 temporary top in AUD/USD and 1.2680 support in USD/CAD. Break of these levels could trigger more buying in Aussie and Loonie.

In Europe, at the time of writing, FTSE is down -1.48%. DAX is down -2.31%. CAC is down -2.95%. Germany 10-year yield is down -0.052 at 0.178. Earlier in Asia, Nikkei rose 0.19%. Hong Kong HSI dropped -0.24%. China Shanghai SSE rose 0.32%. Singapore Strait Times dropped -1.59%. Japan 10-year JGB yield dropped -0.023 at 0.185.

US goods trade deficit widened to USD 107.6B in Jan

US goods exports dropped USD -2.8B to USD 154.8B in January. Goods imports rose USD 4.4B to USD 262.5B. Trade deficit widened by USD -7.2B to USD -107.6B, larger than expectation of USD -98.5B. Wholesale inventories rose 0.8% mom to USD 798.2B. Retail inventories rose 1.9% mom to USD 658.1B.

From Canada, current account balance turned into CAD -0.8B in Q4. IPPI rose 3.0% mom in January while RMPI rose 6.5% mom.

ECB Panetta: The world becomes darker, our steps should be smaller

ECB Executive Board member Fabio Panetta said, “we should adjust policy carefully and recalibrate it as we see the effects of our decisions, so as to avoid suffocating the recovery,” he said.

Talking about Russia invasion, he said, “this terrible event has made the need for prudence even greater. The world has become darker, and our steps should be smaller still.”

“The most important thing right now is for us to be ready and available to preserve financial stability,” he added.

ECB Centeno: Stagflation risks increased with Russia invasion of Ukraine

ECB Governing Council member Mario Centeno “I am convinced that the traction of growth that the economy was following will prevail.” But, “a scenario close to stagflation is not out of the possibilities that we can face. So we need to adjust our policies to that.”

He added that policymakers had already considered the threat of stagflation before. “After the invasion these risks have only increased,” he said. Russian’s invasion of Ukraine has the possibility of “a positive impact on inflation, a few decimal points, and a negative impact on growth.”

Swiss KOF dropped to 105 in Feb, primarily on manufacturing

Swiss KOF Economic Barometer dropped from 107.2 to 105 in February, below expectation of 108.5. KOF said, “the indicators from the manufacturing sector are primarily responsible for the decline, followed by those from the financial sector. The signals for the Swiss exporters are somewhat more favourable than before. ”

Also released, retail sales rose 5.1% yoy in January, versus expectation of 0.4% yoy. GDP grew 0.3% qoq in Q4, below expectation of 0.4% qoq.

Japan industrial production dropped -1.3% mom in Jan, retail sales rose 1.6% yoy

Japan industrial production dropped -1.3% mom in January, worse than expectation of -0.7% mom. Output declined for the second month, after the -1.0% mom contraction in December. Production of cars and other motor parts slumped -17.2% mom, falling for the first time in four months.

Nevertheless according to survey by the Ministry of Economy, Trade and Industry (METI), output is expected to bounce back by 5.7% mom in February and 0.1% mom in March. But the forecasts were taken before Russia’s invasion of Ukraine, which impact is still unknown.

Retail sales rose 1.6% yoy, above expectation of 1.1% yoy, fourth consecutive month of expansion.

Australia retail sales rose 1.8% mom in Jan, above expectation

Australia retail sales rose 1.8% mom in January, above expectation of 0.4% mom.

Director of Quarterly Economy Wide Statistics, Ben James said: “The emergence of the Omicron variant and rising COVID-19 case numbers, combined with an absence of mandated lockdowns has resulted in a range of different consumer behaviours. We have seen the type of spending previously associated with lockdowns occurring simultaneously with those associated with the easing of lockdown conditions.”

“This had led to variations across the industries with Food retailing recording a rise in sales consistent with previous COVID-19 outbreaks as consumers exercise caution amidst surging case numbers. However, the absence of lockdowns meant that other discretionary industries which would usually see a fall during the pandemic have recorded mixed results.”

Also released, private sector credit rose 0.6% mom, versus expectation of 0.7% mom.

New Zealand ANZ business confidence dropped to -51.8, a challenging year in 2022

New Zealand ANZ business confidence dropped to -51.8 in February, down from December’s -23.2. Own activity outlook dropped from 11.8 to -2.2. Export intentions dropped from 8.8 to 0.9. Investment intentions dropped from 11.4 to 4.5. Employment intentions dropped from 10.5 to 2.3. Cost expectations rose from 88.2 to 92.0. Profit expectations dropped from -13.1 to -32.7. Pricing intentions rose from 63.6 to 74.1. Inflation expectations rose from 4.42 to 5.29.

ANZ said, “All up, 2022 is shaping up to be a challenging year economically, and getting on top of super-charged inflation without an outright recession is looking increasingly difficult. But with CPI inflation heading well over 6% the RBNZ has no choice but keep right on hiking. And now global geopolitical developments threaten yet more imported inflation via energy markets. Buckle up.”

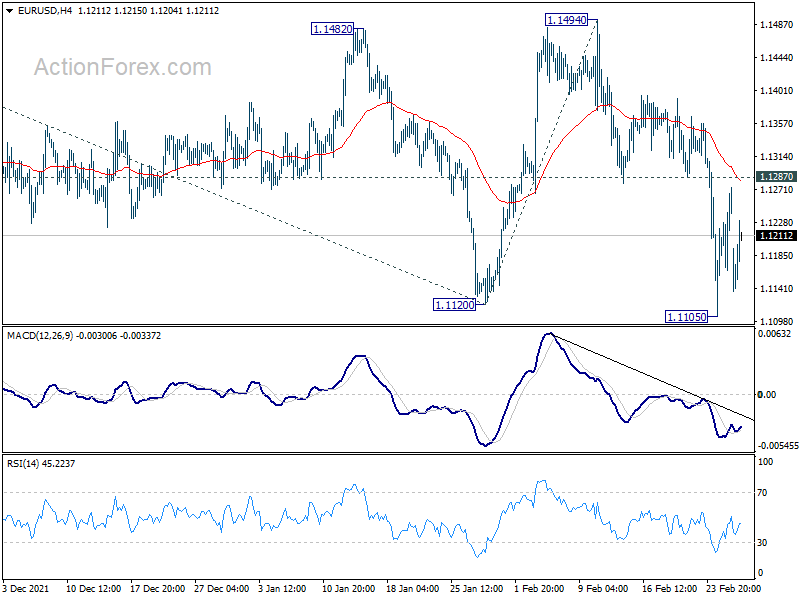

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1201; (P) 1.1238; (R1) 1.1309; More…

EUR/USD is staying in consolidation above 1.1105 and intraday bias remains neutral at this point. On the downside, sustained break of 1.1120 will confirm resumption of larger down trend from 1.2348. Next target is 61.8% projection of 1.2265 to 1.1120 from 1.1494 at 1.0786. However, firm break of 1.1287 will dampen this bearish view and turn bias back to the upside for 1.1494 resistance.

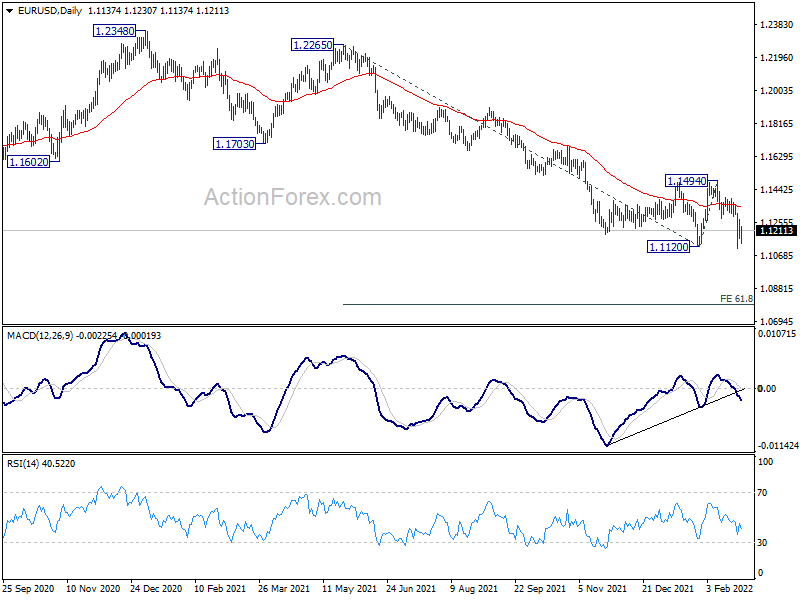

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1582) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

Disclaimer: The views expressed are solely those of the author and do not represent the official position of Followme. Followme does not take responsibility for the accuracy, completeness, or reliability of the information provided and is not liable for any actions taken based on the content, unless explicitly stated in writing.

-THE END-