The latest monthly employment, CPI and retail sales readings are due out of the United Kingdom on Tuesday, Wednesday and Friday, respectively, at 07:00 GMT. The pound is looking somewhat neutral lately as the Bank of England was hawkish, but not hawkish enough at its last meeting. The data will therefore likely be vital in reviving some bullish momentum for sterling as central banks race to remove accommodation from liquidity-fuelled economies.

Not hawkish enough?

When the Bank of England lifted rates earlier this month, it surprised markets as four Monetary Policy Committee members voted for a 50 basis points increase instead of 25 basis points. However, while it’s almost certain the BoE will raise interest rates at least a few more times in its upcoming meetings, the rate hike path becomes a little less clear moving towards the end of the year and into 2023. According to the Bank’s forecasts, there’s a risk inflation will undershoot the 2% target in three years’ time even if energy prices were to remain at current levels.

This implies that policymakers don’t see the Bank Rate peaking very high, which puts the pound at a disadvantage compared to currencies like the US dollar as there’s a strong likelihood the Federal Reserve will end up raising borrowing costs well above UK ones. Another dampener for sterling has been Governor Andrew Bailey’s preference to move in 25bps increments – a view that Chief Economist Huw Pill also shares. Thus, as long as the MPC remains split 50-50, Bailey, who has the casting vote, is unlikely to side with the more hawkish members.

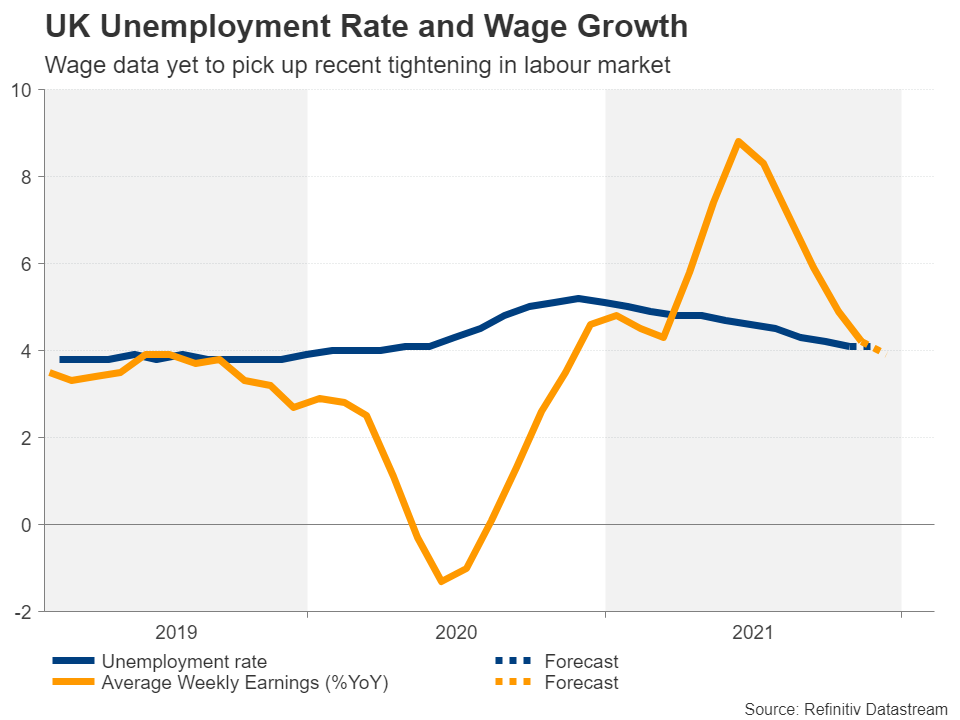

A tight labour market

However, although there’s a sizeable downside risk to inflation if the energy crisis were to dissipate soon, there are equally upside risks to the price outlook in the UK. One of those risks is from the tight labour market.

Jobs growth in the UK is expected to have slowed in the three months to December, while the unemployment rate is projected to have stayed unchanged at 4.1%. Investors will also be looking at the wage growth figures as well as the more up-to-date claimant count measuring the change in number of job seekers on unemployment benefits in January. Average weekly earnings are forecast to have risen by 3.9% year-on-year, decelerating from the 4.2% pace in November.

Economic activity was constrained by the Omicron wave in both December and January so stronger-than-expected showings in jobs and wage growth during the period could boost bets of more aggressive rate hikes by the BoE over the next few months.

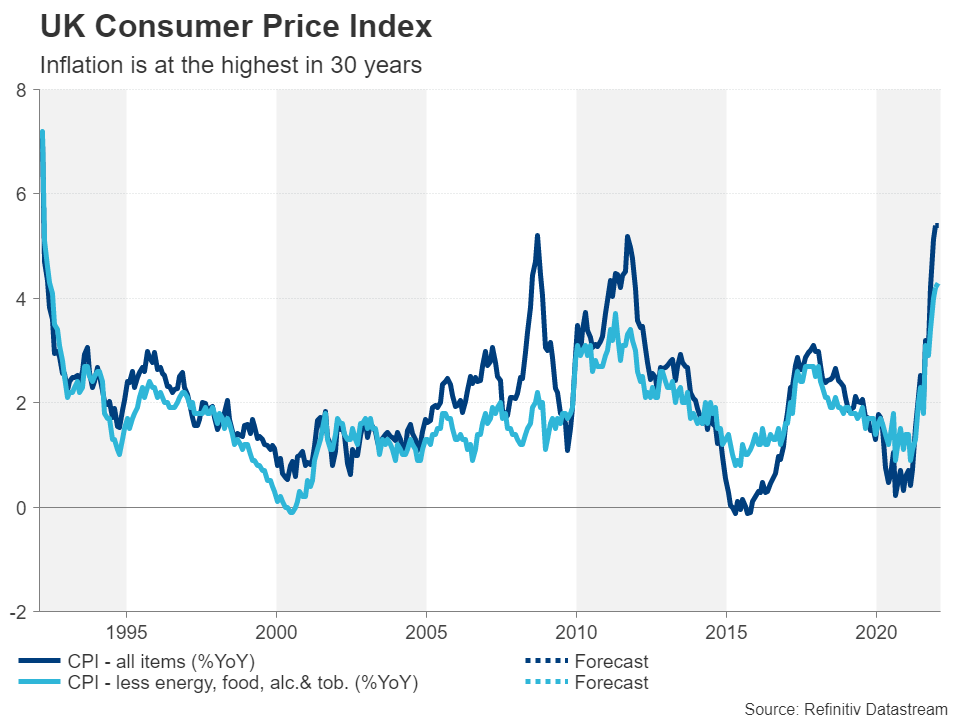

Too early to get excited about slowing inflation

Moving on to the more crucial CPI numbers, there might be some signs that UK inflation has started to peak. The headline consumer price index is projected to have held steady at 5.4% y/y in January. Core CPI is forecast to have continued to edge up, though, rising to 4.3% y/y from 4.2% in December.

If headline inflation does appear to moderate, it is likely to be only a temporary reprieve as energy bills are set to soar in April when electricity providers will be able to charge much higher prices following the UK regulator’s decision to raise the price cap.

Finally, retail sales are expected to have bounced back in January following a 3.7% plunge in December. Retail sales probably recovered by 0.6% month-on-month, which wouldn’t be enough to make up for the prior month’s drop but would nevertheless point to an improving picture for consumption.

Pound stumbles as tightening race gets crowded

Money markets are currently pricing in around six additional 25-bps rate increases for the rest of the year so a solid set of data could push up those odds even further. However, with many expecting the Fed to hike almost seven times, there might be limited upside for sterling.

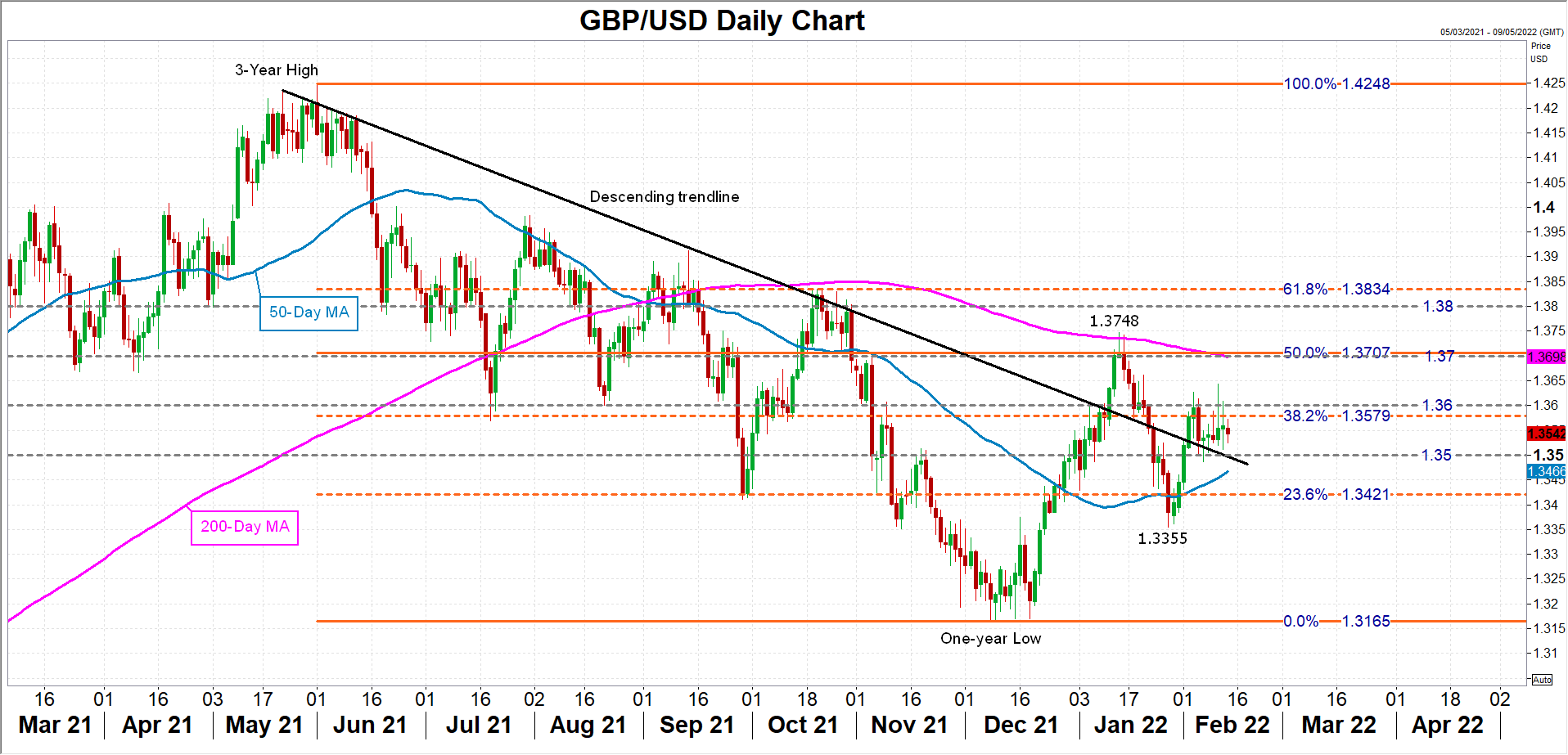

Pound/dollar has managed to hold above its descending trendline despite the greenback’s extreme choppiness of late. A fresh data-driven bull run could bring the critical $1.37 level into scope, which not only coincides with the 200-day moving average, but also the 50% Fibonacci of the May-December 2021 downtrend.

However, should the incoming releases disappoint, a pullback towards the January low of $1.3355 is possible, which would result in a breach of both the descending trendline as well as the 50-day moving average.

In the bigger picture, cable needs to surpass the January top of $1.3748 if it is to switch to a more bullish outlook. But with Bailey favouring a measured response to fighting inflation, the pound may not gain much additional bullish traction unless the CPI prints for January and beyond come in significantly hotter than expected.

Disclaimer: The views expressed are solely those of the author and do not represent the official position of Followme. Followme does not take responsibility for the accuracy, completeness, or reliability of the information provided and is not liable for any actions taken based on the content, unless explicitly stated in writing.

Leave Your Message Now