US inflation: Increasing discomfort

Annual inflation has reached 5.3% in the US in June. Its drivers are still very concentrated but there is concern that they will spread. Anecdotal evidence is accumulating that price pressures faced by companies are increasing. Price pressures as reported in the ISM survey send the same signal. Historically, they have been highly correlated with producer price inflation and consumer price inflation but the transmission depends on factors such as pricing power, competitive position, labour market bottlenecks, etc. The next several months will be crucial for the Federal Reserve and for financial markets, considering the Fed’s conviction that the inflation increase should be temporary. The bond market has bought into this view thus far but, going forward, its sensitivity to upside surprises to inflation should be higher than normal.

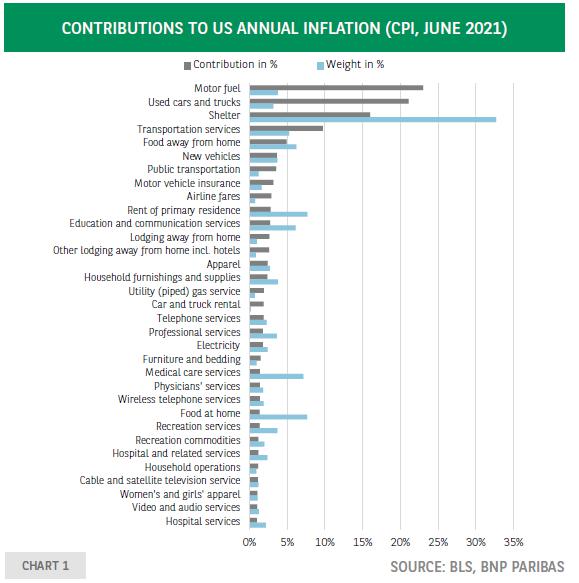

Forming an opinion solely based on anecdotal evidence may be risky but judging by recent comments from companies, something seems to be happening in terms of inflation. The CEO of car manufacturer Stellantis sees “inflation coming from many different areas.”1 The CEO of consumer goods company Unilever was quoted by the Financial Times saying that the company is “facing its fiercest inflationary pressures in a decade as the cost of raw materials, packaging and transport soars.”2 Restaurant chain Chipotle Mexican Grill has warned that “higher beef and freight costs will offset the benefit of menu price hikes in the near term.”3 These quotes confirm the signal from the purchasing managers’ indices, which, for several months already and in most countries, show elevated price pressures – both input and output prices – and lengthening delivery lags. The issue is of particular importance in the US, given its potential impact on Federal Reserve policy, which in turn could have global repercussions. The latest Beige Book – which has been prepared ahead of the FOMC meeting on 27-28 July – reported above-average pay increases for low-wage earners, broad-based pricing pressures as well as above-average price increases. In June, annual consumer price inflation reached 5.3% but the drivers are still very concentrated. Close to 80% is explained by the cost of motor fuel, used cars and trucks, shelter, transportation services, food away from home and new vehicles (chart 1). It shows the influence of the unleashing of pent-up demand and supply bottlenecks. It explains why the Federal Reserve considers the inflation increase to be temporary: demand growth should slow and supply should increase.

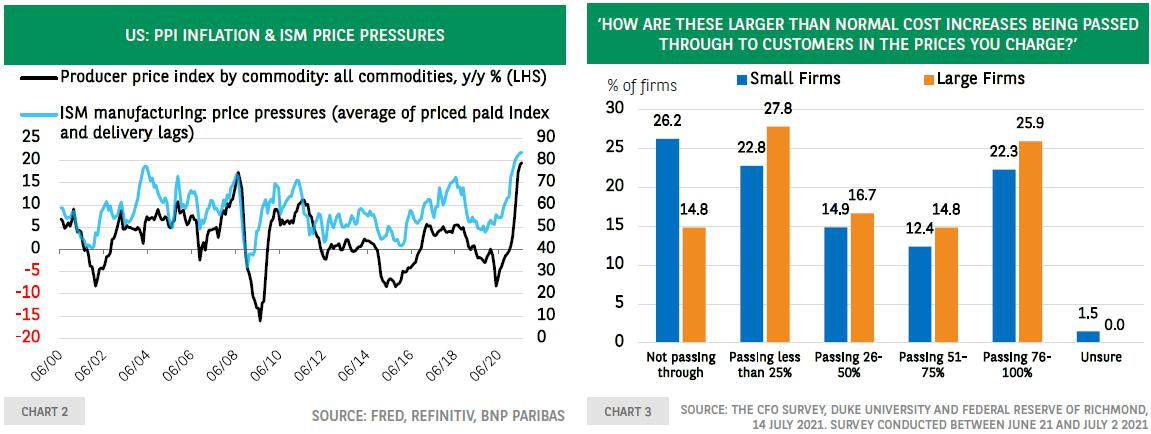

Assessing the possible dynamics of inflation is a challenge because so many factors are at play. Consumer prices concern products and services at the end of a sometimes long supply chain. How quickly and how much will a price impulse observed upstream be transmitted into price developments midstream – the producer price index (PPI) – and downstream, at the level of the CPI? For a qualitative assessment of this transmission, it is useful to start from the PPI. The change in this index corresponds to the sum of changes in profit margins per unit of production, unit labour costs, taxes minus subsidies and intermediate inputs. The elevated level of the ISM-based price pressure indicator – the average of the prices paid component and the length of the delivery lags – suggests that intermediate input price inflation is ikely to remain high for some time. This is also the message from the Beige Book: “while some contacts felt that pricing pressures were transitory, the majority expected further increases in input costs and selling prices in the coming months.” Historically, quite a close relationship can be observed between the price pressure indicator and producer price inflation (chart 2). The evolution of unit labour costs depends on factors like inflation expectations, labour market tightness – reflected in attractive job opportunities – and negotiation power as well as productivity. According to the Beige Book, wages are, on average, increasing at a moderate pace but the low-wage workers are benefitting from above-average increases. In some parts of the country staff turnover is higher than normal. Eventually, this may eat into profit margins, unless companies feel comfortable about raising prices. Reports on certain companies point in that direction, but according to the Beige Book pricing power is mixed. The quarterly CFO survey of Duke University and the Federal Reserve of Richmond shows that most companies pass through to their customers part of their cost increases but the percentages differ greatly (chart 3). This is partly related to their market power and price adaptation strategies.

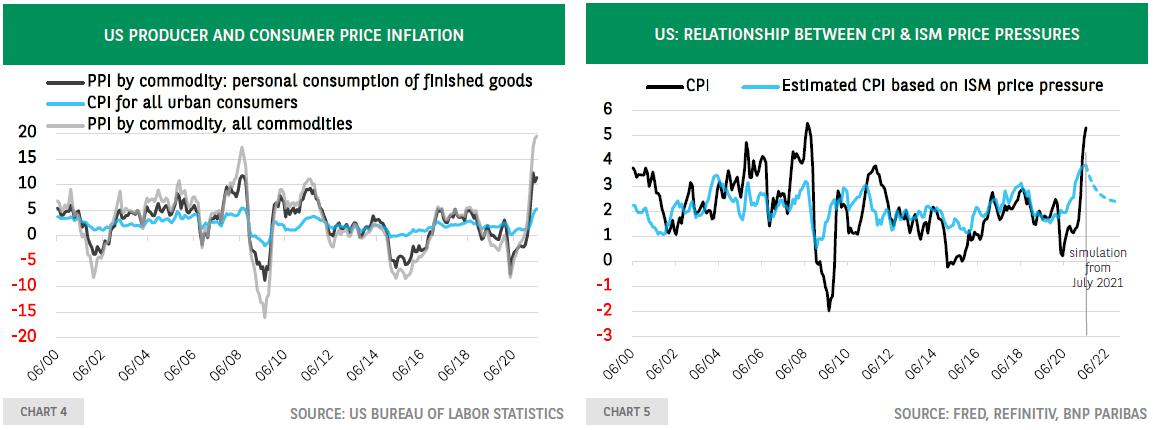

Moving from the PPI to the CPI, one should be aware of the many differences between the two indices. The former concerns domestic production whereas the latter reflects the cost of the consumer basket and includes imported final goods. In addition, distribution costs and profits margins at the wholesale and retail level are part of the CPI. These and other differences such as menu costs explain why the cyclical amplitude of consumer prices is smaller than for producer prices, although the correlation is quite high (chart 4). Given the relationships between the price pressure indicator and producer price inflation and between the latter and consumer price inflation, what do price pressures tell us about the CPI? A simple regression shows that, although the relationship is statistically significant, it only tells (a small) part of the story4. With this caveat in mind, chart 5 provides a back of the envelope simulation of a scenario where the ISM price pressures would drop to 60 at the end of 20225. This would bring consumer price inflation back to 2.4%.

To conclude, US inflation has increased significantly from 2.3% before the Covid-19 crisis to 5.3% by June 2021, and business surveys show that companies expect further increases in input prices. This reflects imbalances between supply and demand, but, based on surveys about pricing intentions, there is a concern that this could spill over to other sectors. Wage growth -another potentially important driver of price pressures- is higher than normal for low-wage jobs but not for the economy as a whole. All this implies that the next several months will be crucial for the Federal Reserve and for financial markets, considering the Fed’s conviction thus far that the inflation increase should be temporary. The bond market has bought into this view, but it implies that, should the assessment change, the reaction could be abrupt. In such an environment, the sensitivity of bond yields to upside surprises to inflation should be higher than normal.

Download The Full EcoFlash

Reprinted from FXStreet,the copyright all reserved by the original author.

Disclaimer: The content above represents only the views of the author or guest. It does not represent any views or positions of FOLLOWME and does not mean that FOLLOWME agrees with its statement or description, nor does it constitute any investment advice. For all actions taken by visitors based on information provided by the FOLLOWME community, the community does not assume any form of liability unless otherwise expressly promised in writing.

FOLLOWME Trading Community Website: https://www.followme.com

Hot

No comment on record. Start new comment.