Focus on the data, but politics still in play

After last week’s focus on US stimulus, Brexit, vaccine roll outs, virus worries, and lockdowns, attention will turn back to fundamentals with heavy data slates around the world. However, politics will still be an issue near term. On the immediate radar are the runoff elections in Georgia which will determine control of the Senate, which in turn will set the legislative agenda for Congress. In the UK, it will be adjustment time after leaving the EU single market, with many Brexit details still to be worked out. Asia’s economic data should continue to reflect the strength of the recovery even at a slightly more moderate pace.

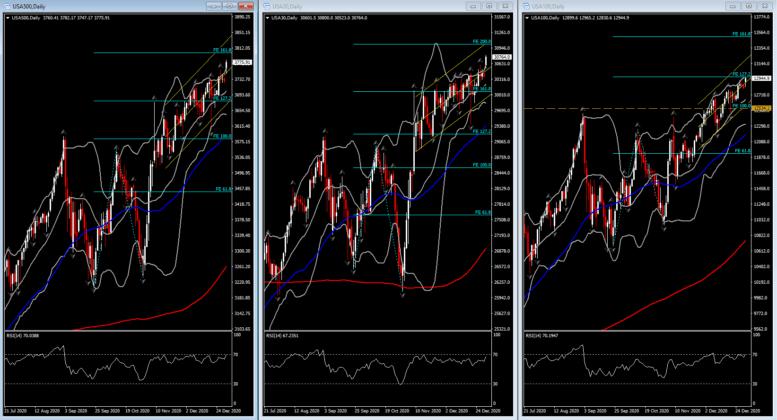

It’s back to work for US markets, kicking off 2021 after the USA30 and USA500 closed out 2020 at record highs. Combined, the major indexes posted 102 fresh peaks through the year. Compared to March lows, the USA30 was 64% higher, the USA500 up 67% and the USA100 a remarkable 88% firmer. Moreover, the rally saw a further broadening of gains as shares of firms that would benefit from a return to normal saw continued buying interest. Concurrently, yields richened in the few weeks leading up to year end after the 10-year and 30-year rates failed to eclipse 1% and 1.75% levels, respectively.

Wall Street and global stock markets added to already impressive gains in December, fueled by the rollout of vaccines that are widely seen as driving a robust recovery in 2021 after the volatile path seen in 2020. Adding to the optimism was the passage of a fresh stimulus bill in the US and a Christmas Eve Brexit agreement. The accumulation of upbeat developments continued to overshadow the challenges facing the economy in the very near term, as surging infections triggered increasingly stringent lockdowns in the US, Europe and parts of Asia, suggesting a rocky start to the year for global growth. Meanwhile, bond markets continued to take a more measured view of the growth outlook, as the uptick in yields since March has sharply undershot the magnitude of the upward trajectory in equities. The tension between dismal near term and sunny medium term outlooks will continue to drive volatility in equity, bond and currency trading as the New Year begins.

Vaccines rolled out in the UK, US and Europe during December, providing the market with a light at the end of the tunnel as infections, hospitalizations and restrictions soared. Front line health care workers and the elderly have priority, but expectations have grown that wider availability will be the case by the middle of the year, if not a bit earlier. Japan will begin to vaccinate in late February, according to a Bloomberg report that cited local media sources.

Meanwhile, President Trump signed a $2.3 tln omnibus spending bill as the month of December came to a close, averting a partial government shutdown and funding the government through September. More importantly for the market, the bill includes $900 bln pandemic relief measures that will add PPP funds, boost extended unemployment benefits and the eviction moratorium, support the airlines, and increase money for vaccine distribution. The bill provides $600 checks to individuals. Congress indicated it would review Section 230 which advantages big tech, and will look into voter fraud issues.

There are a number of key economic reports on tap this week, including ISMs and vehicle sales, though culminating with the December employment data. The Fed is back in focus too with the FOMC minutes and Fedspeak due.

The December jobs report should garner extra attention given the non-trivial risk of a drop in payrolls as restrictions ratcheted up on the spikes in virus infections since November and the delayed stimulus. Of course, the service sector again suffered the brunt of the restrictions, but that sector has already been hollowed by the spring shutdowns, so weakness may be tempered. Hence, a 100k December nonfarm payroll increase is expected, after gains of 245k in November, 610k in October, and 711k in September. We also note that initial claims are not flashing warnings signs about employment in December — claims fell -19k to 787k in the Christmas week, extending the -86k plunge to 806k in the prior week. The jobless rate should tick up to 6.8% from 6.7% in November, versus a 14.7% peak in April. Average hourly earnings should increase 0.2%.

Fed policy will be on view again after the holiday hiatus. The FOMC released the minutes to its December 15-16 meeting the results of which were uneventful as the 0% to 0.25% rate band was maintained, and there were no changes to QE. However, the minutes will be scrutinized for insights into the general thinking of policymakers. Note there is a new voting rotation this year, and the new crew of Evans, Bostic, and Daly will tilt to the dovish side, with just Barkin more of a centrist. And Fedspeak this week will include the aforementioned doves. Also on tap are Williams, Mester, Harker, Bullard, and VC Clarida.

Reprinted from FXStreet,the copyright all reserved by the original author.

Disclaimer: The content above represents only the views of the author or guest. It does not represent any views or positions of FOLLOWME and does not mean that FOLLOWME agrees with its statement or description, nor does it constitute any investment advice. For all actions taken by visitors based on information provided by the FOLLOWME community, the community does not assume any form of liability unless otherwise expressly promised in writing.

FOLLOWME Trading Community Website: https://www.followme.com

Hot

No comment on record. Start new comment.