The forex markets are relatively steady in Asian session today, despite strong moves in stocks and treasury yields overnight. Australian Dollar is treading water after RBA left monetary policies unchanged. It’s clear that the central is paving the way for more easing to support the job market. But the statement left traders wondering the timing and extent of the next move. Dollar remains weak and it would take some more time to see if surging yield could finally give the greenback a hand.

Technically, EUR/USD’s break of 1.1769 resistance is sign of bullish reversal in the pair. EUR/JPY also resumed the rally rebound from 122.37. Yet, we’re not seeing clear downside breakout in Dollar pairs yet, including GBP/USD and AUD/USD. GBP/JPY’s break of 137.00 is a sign of more upside in Yen crosses in general. But we’re also not seeing equivalent upside breakout in USD/JPY. The overall pictures are rather mixed, except that European majors seem to be having an upper hand for now.

In Asia, currently, Nikkei is up 0.47%. Hong Kong HSI is up 0.75%. Singapore Strait Times is up 0.55%. Japan 10-year yield is up 0.0089 at 0.035. China is still on holiday. Overnight, DOW rose 1.68%. S&P 500 rose 1.80%. NASDAQ rose 2.32%. 10-year yield rose 0.066 to 0.762.

RBA: Addressing unemployment an important national priority, considers additional monetary easing

RBA left monetary policy unchanged as widely expected. Cash rate and 3-year Australian Government bond yield target are held at 0.25%. The parameters for the expanded Term Funding Facility is also kept unchanged.

Nevertheless, in the statement, RBA emphasized that “addressing the high rate of unemployment as an important national priority.” It reiterated the pledge to “maintain highly accommodative policy settings as long as required. Also, it “will not increase the cash rate target until progress is being made” on employment and inflation.

Additionally, “the Board continues to consider how additional monetary easing could support jobs as the economy opens up further.”

Also from Australia, exports of goods and services dropped -4% mom to AUD 32.6B in August. Imports of goods and services rose 2% mom to AUD 30.0B. Trade surplus shrank to AUD 2.64B, down from July’s AUD 4.61B, missed expectation of AUD 5.05B.

US 10-year yield posted strong rise, hit highest level since Jun

US treasury yields at the long end also posted strong rally. 10-year yield closed up 0.066 at 0.762, hitting the highest level since June. There were a couple of explanations for the strong move. There appeared to be progress on the prospect of a fresh stimulus deal before election, especially after President Donald Trump contracted the coronavirus himself. Also, some noted that Democratic challenger Joe Biden’s lead is paving the way for bigger government spending, and deficit, after the election.

At the same time, we could also argue Trump’s speedy recovery showed huge progress in coronavirus treatment, which is the single most determinant factor for the economic course onwards. Additionally, Fed officials are clearly in unison to drive inflation overnight in the next couple of years.

In any case, 10-year yield should now be leading 55 day EMA behind while rise from 0.504 resumes. 0.957 resistance would be the next target. Though, we don’t expect a break there any time soon.

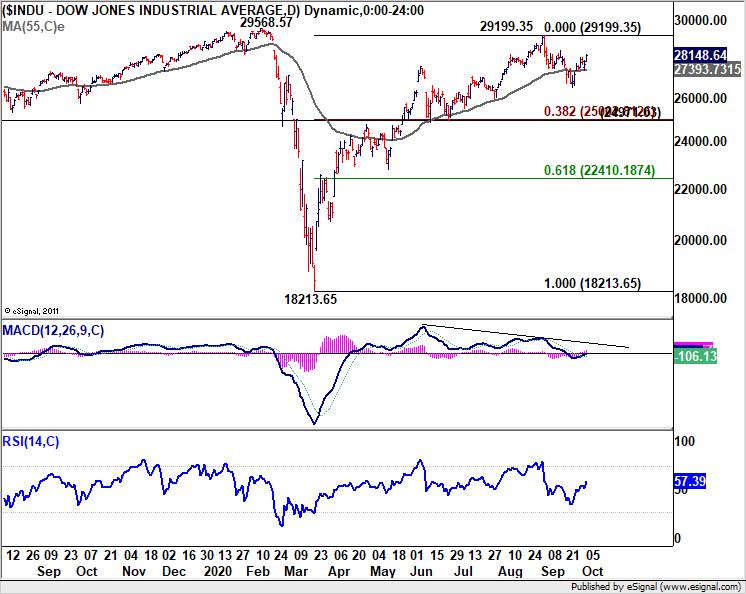

DOW broke last week’s high

US stock also closed with strong gains. DOW and S&P 500 led this time, breaking through last week’s high while NASDAQ lagged. Clear support is seen from 55 day EMA (now at 27393.73) for now. Further rise should be seen to retest 29199.35 in the near term. Though, we’re not expecting a clean break there yet. Another fall is still likely before the consolidation from 29199.35 completes.

Fed Evans quite pleased if core inflation could hit 2.5% for a time

Chicago Fed President Charles Evans said yesterday that inflation has to “cross over, beyond 2%, with some momentum”. He’d be “quite pleased” if Fed could get core inflation up to “2.5%” for a time.

He expects inflation to “slowly improve, reaching 2% on a persistent basis in 2023 and then moderately overshooting 2% over the following few years”. He didn’t expect unemployment to come back to 4% until 2023.

“My forecast assumes that additional federal fiscal policy actions are coming,” Evans added. “Without adequate fiscal support before too long, I am concerned that recessionary dynamics will gain more traction and lead to a slower trajectory back to maximum employment.”

Looking ahead

Germany factor orders will be released in European session. UK will release PMI construction. US and Canada will release trade balance.

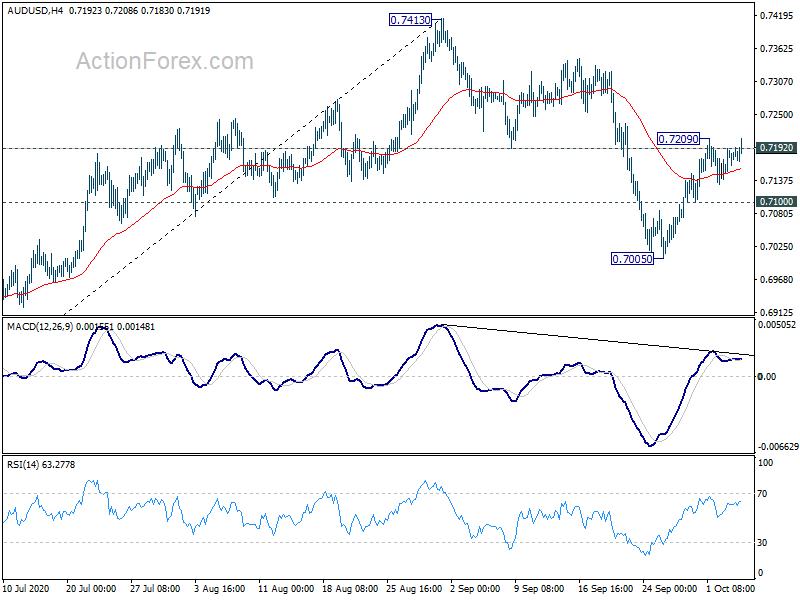

AUD/USD Daily Report

Daily Pivots: (S1) 0.7163; (P) 0.7178; (R1) 0.7197;

Intraday bias in AUD/USD remains neural for the moment. On the upside, break of 0.7209 and sustained trading above 0.7192 should confirm completion of the pull back from 0.7413. Further rise should be seen back to retest 0.7413 high. On the downside, below 0.7100 minor support will turn bias back to the downside for 0.7005 support. Break of 0.7005 will resume the correction from 0.7413 to 38.2% retracement of 0.5506 to 0.7413 at 0.6685.

In the bigger picture, while rebound from 0.5506 was strong, there is not enough evidence to confirm bullish trend reversal yet. That is, it could be just a corrective inside the long term up trend. Sustained trading back below 55 week EMA (now at 0.6908) will favor the bearish case and argue that the rebound has completed. Focus will be turned back to 0.5506 low. On the upside, break of 0.7413 will extend the rise from 0.5506 to 38.2% retracement of 1.1079 (2011 high) to 0.5506 (2020 low) at 0.7635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Sep | 45.2 | 37.9 | ||

| 0:30 | AUD | Trade Balance (AUD) Aug | 2.64B | 5.05B | 4.61B | |

| 3:30 | AUD | RBA Rate Decision | 0.25% | 0.25% | 0.25% | |

| 6:00 | EUR | Germany Factory Orders M/M Aug | 3.00% | 2.80% | ||

| 8:30 | GBP | Construction PMI Sep | 58.5 | 54.6 | ||

| 12:30 | CAD | Trade Balance (CAD) Aug | -2.5B | |||

| 12:30 | USD | Trade Balance (USD) Aug | -66.2B | -63.6B |

Hot

-THE END-